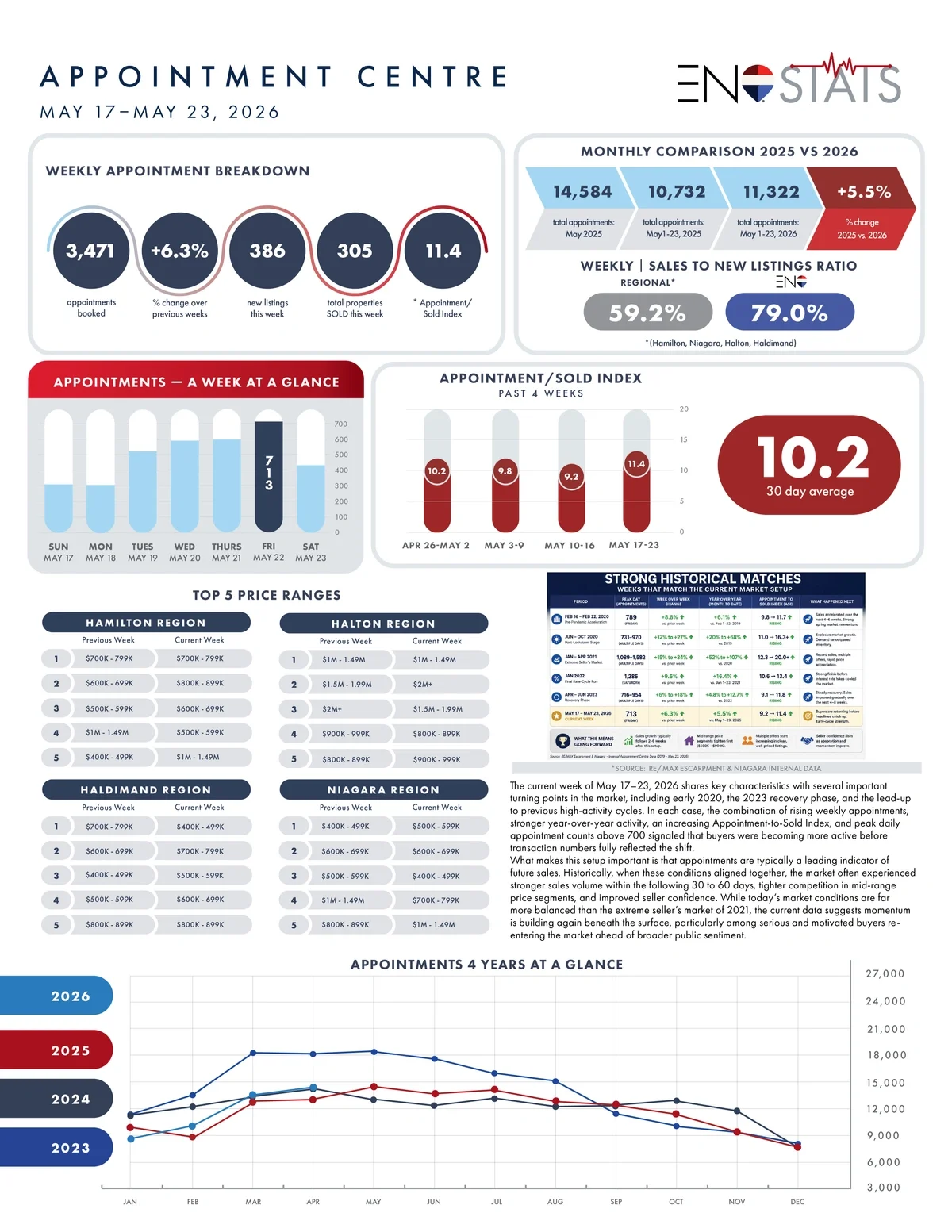

The current week of May 17–23, 2026 shares key characteristics with several important turning points in the market, including early 2020, the 2023 recovery phase, and the lead-up to previous high-activity cycles. In each case, the combination of rising weekly appointments, stronger year-over-year activity, an increasing Appointment-to-Sold Index, and peak daily appointment counts above 700 signaled that buyers were becoming more active before transaction numbers fully reflected the shift.

What makes this setup important is that appointments are typically a leading indicator of future sales. Historically, when these conditions aligned together, the market often experienced stronger sales volume within the following 30 to 60 days, tighter competition in mid-range price segments, and improved seller confidence. While today’s market conditions are far more balanced than the extreme seller’s market of 2021, the current data suggests momentum is building again beneath the surface, particularly among serious and motivated buyers re-entering the market ahead of broader public sentiment.